If you are a landlord with less than 3 properties, which you are letting out in the UK, then this guide will give you a thorough grasp of the basics of property tax and capital gains tax in the UK.

If you have more than 3 properties we expect that you would already know about the basics or that you have a tax adviser who handles it all for you. If you do not and are not being advised, then please, get in touch… quickly. We have written the guide to give UK Landlords a straight forward understanding of the current tax rules as they apply to property before letting, whilst letting and on selling property in the UK.

We particularly hope it answers the many questions we get asked every day from those landlords who are new to letting and unused to dealing with HMRC and the way our tax system works outside of PAYE. The guide should take you no more than 30 minutes to read from start to finish.

Taxation of Property

Income from property for individuals is assessed to income tax for each tax year. Records therefore need to be kept for each year ending on 5th April. Married couples or civil partners who let their property out jointly are usually assessed on one half of the income, unless they actually legally share the profit in unequal shares and make a formal election to HMRC. Where property is jointly owned it is not usually treated as a partnership, unless there is a trading activity as well. The accounting period for partnerships and limited companies do not have to end on 5th April.

Types of UK Property

Commercial Property

This is a property which is not residential including land. If you let out part of your business accommodation because it is temporarily surplus to current business requirements, then the income and expenses, as long as they meet the conditions, can be treated as trading profits. The advantage is that it becomes pensionable earnings but it is then income assessable to Class 4 National Insurance.

Furnished Holiday Lettings

There are special rules for furnished holiday lettings. The advantage is that any Capital Gains on the sale of the property are eligible for Business Asset Disposal Relief, Hold-over relief or Roll-over relief. To qualify, the property must be let commercially for at least 105 days and available for at least 210 days in any tax year. There are elections which may assist if the qualifying days are not reached in a particular year. If, the property is let to the same person for more than 31 days at a time, this period is not included. Further if the total of any periods that it is let for more than 31 days exceeds 155 days in a tax year then the property does not qualify as a furnished holiday letting. Losses from furnished holiday lettings can no longer be set against other income.

Rent a Room

If you let out a furnished room in your home, provided it is not an office, Rent a Room relief can be claimed rather than paying tax on the net profit. Rent a room relief was increased significantly from 6th April 2016 to a fixed figure of up to £7500 p.a. per household or £3750 p.a. each for a couple and is deducted from the gross rents received. You cannot deduct any expenses if you claim Rent a Room relief nor can it create a loss. It is simpler than apportioning all the home expenses and is normally more beneficial.

Other Residential Lettings

These will be other lettings which do not qualify as furnished holiday lettings or you are not claiming Rent a Room relief. From 6th April 2016 there is a new relief for actual expenditure on replacement furnishings. Relief cannot be claimed for expenditure on new capital items which are not replacements on a like for like basis.

| Property Type | Revenue Expenses | Capital Allowances | Replacement Furniture Relief | Loss Relief against Income |

|---|

| Commercial Property | √ | √ | × | ∗ |

| Furnished Holiday Lettings | √ | √ | × | × |

| Rent a Room | × | × | × | × |

| Other Residential Lettings | √ | × | √ | × |

∗ Loss relief against other income may be available if created by surplus capital allowances

Accounting for Rental Income and Expenses

Income and expenses are accounted for on a cash basis, provided that the total gross income does not exceed £150,000. Income and expenses are accounted for on an arising basis if you elect for this basis or the gross income is above £150,000

Rental Income

Any rental income received should be declared gross before the deduction of any agent’s fees which should be included as an expense. Any deposits received have to be safeguarded by an approved scheme or will be dealt with by your agent. Deposits received should not be included in your income.

There are some specific rules for agricultural tenancies which are not included below.

Property Income Allowance

The property income allowance of £1000 can be deducted from your rental income (provided that the income is not received from a connected party) instead of any expenses. It is only worth claiming this allowance if your expenses are less than £1000 and they are less than the actual rent received. You cannot claim any expenses if you claim the Property Income Allowance. The allowance is designed to save people with low rental income having to declare and pay tax on that income rather than as a general tax saving measure.

Expenses that CAN be Deducted against Rental Income

The general rule is that the expenditure must be expended wholly and exclusively for the Rental Income business. The rules are exactly the same as trading expenses.

Finance costs (restricted for other residential lettings)

The interest paid and arrangement fees on any loan taken out to purchase or improve the rental property together with any bank charges on a separate rental property bank account are finance costs. If it is a repayment mortgage, then it is only the interest element which counts as finance costs not the total repayments.

For commercial properties, Furnished Holiday Lettings (see above) and residential properties owned by limited liability companies, the finance costs are allowed in full.

For other residential properties owned by individuals or partnerships, the finance costs are restricted and only 20% of the finance costs can be claimed against the tax liability on the net rental income after deducting all other expenses and losses brought forward but before any finance costs.

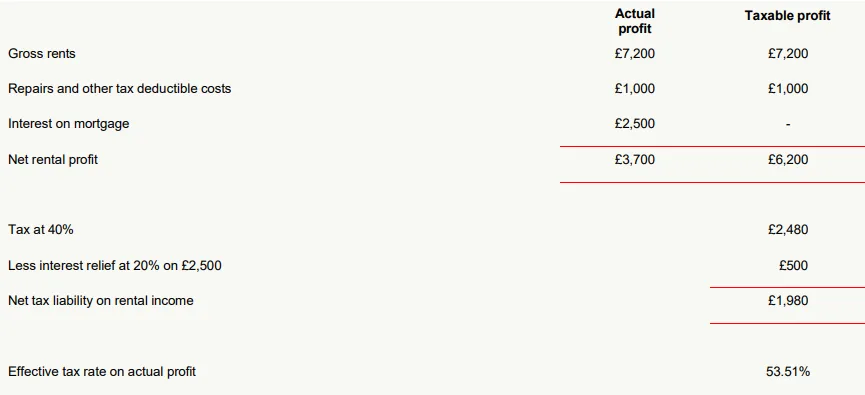

The best way of explaining this is by way of an example:

Joe is a teacher and is 49 years old; he is a 40% taxpayer. He has purchased a buy to let residential property as an investment. As he has owned the property for some time, the outstanding debt on the property is relatively low. This is how the finance costs are treated:

As you can see the effective rate of tax is 53.51% which is more than Joe’s marginal rate of 40%. Where landlords are highly geared, the tax liability could be more than the net rental income received.

Basic rate (20%) taxpayers should effectively receive full relief provided that the rental income before interest does not cause them to go into the higher rate of tax.

Higher rate taxpayers may wish to consider purchasing new properties in a limited company as finance costs are allowable in full. However, lenders do tend to charge a higher rate of interest on loans to limited companies.

Repairs and maintenance

Repair work carried out on the property can be claimed provided that it is not a capital improvement. If you lived in the property prior to letting it, then work carried out before the property is let is seen as maintenance of the property as a result of private use rather than for rental purposes. Do not forget to include the gas safety certificate cost if applicable.

Legal, management and accountancy fees

You cannot claim any legal fees in connection with the purchase of the property or any fees for the initial lease if it is for more than one year. Any legal fees in connection with the renewal of a lease, a shorthold tenancy of less than 1 year, eviction of clients, rent collection or management fees and accountancy are all claimable.

Insurance

It is important that you insure the property and the premium for the buildings and/or contents can be claimed. Life assurance premiums are not claimable.

Rent rates and council tax.

You may pay ground rent if the property is a flat. The tenant normally pays the rates or council tax, but if you suffer any costs or there are any void periods where you pay these costs, these can be claimed.

Services

If you pay any service charges or for any other services in connection with the letting e.g. electricity in common areas, these should be claimed. If the property is a furnished holiday letting then it is likely that you will pay for electricity, gas, water, television licence, telephone and other services.

Wages

If you need someone to carry out a regular service for you e.g. cleaning, we recommend that you pay a fixed rate for that service and do not provide any tools or materials so that they can be treated as self-employed. However, if for example, you employ a cleaner for one hour a week and provide all the materials, then that person is probably an employee. Be aware, that if you do employ an employee, you need to ensure that you comply with Employment Regulations including Working Time Directive, National Minimum Wage, Health and Safety, auto enrolment for pensions and PAYE/NIC. The national living wage from 1st April 2023 is £10.42 per hour for adults over age 25. We advise that you should ask your employee to complete a “Starter Checklist” which is available on the Government website https://www.gov.uk/government/publications/paye-starter-checklist. Provided that you do not pay £123 after 6th April 2023 or more per week, you have no other employees and your employee marks either certificate A or B, you can retain the Starter Checklist and take no further action. If certificate C or no box is marked or you pay £123 or more per week it will be necessary to have a PAYE scheme in place. If you have a PAYE scheme then you will need to pay the employee under RTI (Real Time Information) even if they earn less than £123 per week.

Travelling expenses

Do you travel to the property to carry out maintenance or deal with issues with the tenants? If so you should claim the cost of travelling. The authorised mileage rate can be claimed which for cars is 45p per mile for the first 10,000 business miles travelled in a tax year and 25p per mile for each subsequent business mile. If you have a managing agent, HMRC consider this to be your place of business rather than your home. The mileage claim does have to be reasonable – if you live in London and spend a week on holiday in Cornwall, popping in for ten minutes to check that the holiday home next door was alright would not make the journey a business trip! If there was a local managing agent for your Cornish property, you would also not be able to claim the mileage from London to Cornwall.

Advertising

If you need to advertise for tenants, then this expense can be claimed

Administration expenses

These can include postage, stationery, telephone calls and other administration expenses. Either a complex calculation has to be made justifying the charge or the following can be claimed depending on the hours worked in an office:

| Number of Hours Worked per Month | Monthly Claim |

|---|

| 25 or more | £10 |

| 51 or more | £18 |

| 101 or more | £26 |

It is unlikely that a charge for using your home as an office can be justified unless you are managing a number of properties yourself.

Other expenses

The licence fee for Houses of Multiple Occupation (HMO) is claimable for example. Any other expenses incurred wholly and exclusively for the property business can be claimed.

Expenses That CANNOT Be Deducted Against Rental Income

Capital Expenditure

The cost of purchasing or improving a residential property (e.g. an extension) cannot be claimed as revenue expenditure against your property income. The distinction between capital and revenue expenditure is not black and white. If you buy a property and simply redecorate it before you let it out, this will be considered to be revenue expenditure. If however you bought a property for a significantly lower price than normal because it was in a poor condition and then carried out substantial works, this expenditure would probably be considered as capital expenditure.

The Structures and Buildings Allowance for non-residential buildings (see below) cannot be claimed for residential properties. However, most capital expenditure is eligible for relief for Capital Gains Tax purposes when you come to sell the property, so it is important that you keep records and receipts for the expenditure incurred.

Any costs and expenses associated with a property purchase which falls through are not allowable. Whilst the interest payable is an allowable deduction, the repayment of any capital on a loan or mortgage raised to purchase/improve the

property cannot be claimed.

Private Use

If you use the property for private purposes, which is most likely if it is a furnished holiday letting or you are not claiming Rent a Room relief in your own home, then any expenditure claimed must be restricted for its private use. If you have previously occupied a property, then any expenditure which relates to that period of occupation cannot be claimed. So, any maintenance of the property prior to the first letting is private. Conversely, if for instance you had paid an annual insurance premium on 1st April and left the property with a view to letting it on the following 1st October, then you would claim one half of the insurance premium paid even though it was paid when you occupied the property.

Capital Allowances (not for Other Residential Lettings)

Capital allowances are available on the purchase of fixtures, plant and machinery. There is an Annual Investment Allowance for expenditure up to £1,000,000 from 1

st January 2019. As most landlords will not be spending more than the annual limit or claiming for a car, cars and eligible expenditure over the annual limit is not discussed.

Examples of expenditure eligible for Annual Investment Allowance are as follows:

| Cookers | Washbasins | Furniture | Storage equipment |

| Washing machines | Sinks | Carpets | Counters |

| Dishwashers | Baths | Curtains | Machinery |

| Refrigerators | Showers | Boilers | Lifts |

| Electrical systems | Water systems | Heating systems | Alarm systems |

The list is not exhaustive and you should obtain further advice from us, particularly if your expenditure is over the annual limit.

If you sell an asset on which you have previously claimed Capital Allowances, the proceeds are taken into account and may create an additional income charge.

Capital Allowances on Other Residential Lettings

Whilst capital allowances cannot be claimed on expenditure on the property, there is limited scope to claim for tools that you use to maintain the property but this does not include tools that you provide to the tenant.

Replacement of Domestic Items Relief

Where a residential property is not a Furnished Holiday let or no Rent a Room relief/Property Income Allowance is claimed, the expenditure on replacing items of furniture and white goods will be allowed as an expense less any proceeds on the disposal of the item being replaced. The cost of assets which are not replacements are not allowed as an expense.

Losses

If the expenses and allowances above are more than the income from the properties, then there will be a loss. Losses are usually only available to carry forward against future property income unless the loss arises from a property which is not let out on a commercial basis.

The interest and other finance charges which are restricted (as outlined above) do not increase the loss. However, if the 20% relief is not used in the tax year then this can be carried forward and used in future years against tax on rental income. It is likely that general losses carried forward on residential properties will reduce significantly as the finance costs are now restricted in full.

Loss Relief against Other Income

Losses on standard residential lets are not allowed against other income. If, however, your losses arise from surplus capital allowances, they can be claimed against other income.

Is it worth having a limited company?

Properties can be held in either in individual name(s) or in a limited company. They can also be held in trusts or non-domestic properties can be held in self-administered pension schemes, which are not dealt with here.

Prior to the restriction on claiming finance charges, unless you intended to hold the properties for a long period and did not need to use the income, we would not have recommend holding your properties in a limited company. This now needs to be considered on an individual basis as it will depend on the amount of interest paid in each case. For a more detailed explanation please see our comprehensive article on this subject

Capital Gains Tax

Basics

In 2008, the calculation of Capital Gains was simplified as follows:

- Proceeds of sale less any selling costs X

- Cost of asset including purchase plus any enhancement expenditure* Y

Capital Gain X-Y

*If the asset was purchased before 31st March 1982 then cost is substituted with the market value on this date plus any enhancement expenditure after this date. For non-residents the market value may be at 5 th April 2015 for residential properties and 5th April 2019 for non-residential properties plus any enhancement expenditure after the relevant date, where the asset was held on the relevant date (see below).

Enhancement expenditure does not include any items of maintenance or finance costs. If you carry out work on a property and then sell it immediately, this may be treated as trading income rather than a capital gain.

Some reliefs are discussed below. After deducting the reliefs there is an annual exemption of £6,000 for 2023/24, reducing to £3,000 for 2024/25 onwards for each individual, which is deducted from the net gains after losses in the tax year. For residential properties/nonresidential properties, tax is then charged at 18%/10% on any surplus basic rate band available for income tax purposes and 28%/20% on the remainder unless Business Asset Disposal Relief can be claimed.

Non UK residents only

Gains on residential properties in the UK arising after 5th April 2015 and land and commercial properties in the UK after 5th April 2019 are taxable on non-residents. Where an asset is held on the relevant date, the default position is that the gain is calculated using the market value of the property at 5th April 2015/2019 as appropriate and deducting it and any enhancement expenditure since the relevant date from the sale proceeds. Alternatively, an election can be made to time apportion or use the actual gain/loss. Where assets are bought after the relevant date, the gain will be calculated in the normal way.

Reporting Capital Gains and paying the tax

UK residents

Non-residential properties

Commercial property sales are reported on your self assessment tax return for the relevant tax year and the tax is payable on 31st January following the end of that tax year.

Residential properties

UK residents are required to report any Capital Gains Tax liability on the disposal of a residential property only and pay any Capital Gains Tax due, within 60 days of the completion date following the disposal. The report and payment must be made using HMRC’s new digital UK Property Service. If you complete a self assessment tax return, the sale will also need to be declared on that return and credit will be given for the tax already paid. You would also use the self assessment tax return to update any estimated figures or if you do not complete a self assessment tax return then the Capital Gains Tax return would need to be amended within 12 months. You do not need to make a report within 60 days if there is no Capital Gains Tax to pay but you will still need to include the details on a self assessment tax return if

it meets the criteria for disclosure.

The disposal of a property which has been used as a principal private residence throughout the period of ownership is exempt and does not have to be reported to HMRC.

Non UK residents

Non-residential properties and Residential properties If you are a non-resident and you dispose of a property in the UK, you must report the gain/loss and pay any Capital Gains Tax due to HMRC within 60 days of the completion date following the disposal. You may also have a liability if you dispose of any other asset and you were to return to the UK within five years of leaving. As with UK residents, you would need to include the gain on your self assessment tax return.

Private Residence Relief

If at any time the property has been your only or principal private residence, then you should be entitled to some private residence relief. Married couples, civil partners and unmarried individuals can only have one principal private residence at a time. If it has been fully used as your only private residence and there has been no letting or other business activity carried on at the premises throughout the period of ownership, normally Private Residence Relief will apply in full. If you incur a capital loss on your principal private residence, then you cannot claim this loss against other gains.

If the property occupies more than ½ hectare (approx. 1.25 acres) then you will have to prove that the additional area is required for the reasonable enjoyment of the property having regard to the size and character of the dwelling otherwise the Private Residence relief will be restricted.

The final nine months (three years if you are disabled or moving into long term care) are treated as eligible for relief whether you were actually living in the premises or not, provided that you have occupied the property as your principal private residence at some time. So, if you leave the property, let it out for nine months and sell it at the end of this period there is no chargeable gain.

Owning more than one residence at a time

If you do have more than one residence which is not let out, then you can elect for one or other to be treated as your principal private residence. This must be done within two years of acquiring the second property and once this has been done, the election can be varied. Both properties must be used by you as a residence, so for example if you have a main residence and a holiday home which you use personally, then you should consider making an election.

If no election is made, then it is a question of fact and generally it is the property that is most lived in. Where there are two properties, some savings in Capital Gains Tax can be made with careful use of the election – although with the reduction in the final period from 36months to 9 months, this is not as advantageous.

If you elect for the second property (under the conditions above) to be your principal private residence and then one week later elect for your normal home to become your main residence again, you will obtain 9 months private residence relief on the sale of the second home. The one week’s capital gain on the main home should be covered by the annual exemption. From 6th April 2015, you cannot elect for a property to be your principal private residence in a particular tax year if it is in a different country to your residence and you have not occupied it for more than 90 days in that tax year.

Business use of your home and lodgers

If you have a study at home, do not use it exclusively for your business otherwise you may have a Capital Gains Tax liability. Any area that has exclusive business use is not eligible for Private Residence Relief and the proportionate gain would be chargeable.

If you let a room in your house to a lodger there will be a restriction on the Private Residence Relief. Although you would then be eligible for Lettings Relief provided that you lived in the property at the same time which could mitigate any CGT liability.

Lettings Relief (mostly withdrawn from 6th April 2020)

Lettings relief is only available if the property has been used by the landlord as a principal private residence and it is occupied by tenants at the same time. The limits on Lettings relief are the lower of the gain, the Private Residence Relief due or £40,000 per individual.

Job related accommodation

If you have to live in job related accommodation for a period, then you can claim principal private residence relief on a dwelling which you own in that period, provided that you have bought it with the intention of living there, even if you let it out.

Living accommodation is job related if:

- it is provided by reason of the individual’s employment, or by reason of the employment of the individual’s spouse or civil partner,

- for the proper performance of their duties, or

- for the better performance of their duties and where the provision of living accommodation is customary for that type of employment, or

- Where the accommodation is provided as part of special security arrangements.

There are anti-avoidance rules which prevent directors of their own companies claiming that accommodation is job related.

Busines Asset Disposal Relief

Business Asset Disposal Relief is available if you dispose of a trading asset or furnished holiday lettings. It could also apply if you sell a commercial property which was used in your trade or by your personal company within the three years prior to disposal. If you are entitled to Business Asset Disposal Relief, then the tax rate reduces from 18/20/28% to 10% of gains up to a lifetime limit of £1 million.

As this relief is not available to most landlords, no further details are given and advice should be sought.

Business asset Rollover Relief

This is available on furnished holiday lettings and on certain trading assets. If you reinvest all or some of your proceeds, you may be able to defer the gain by claiming rollover relief. As this relief is not available to most landlords, no further details are given and advice should be sought.

Annual Tax on Enveloped Dwellings (ATED)

(Limited companies only)

Where a company owns a residential property which is valued at more than £500,000, it must complete an ATED return as at 1st April each year by 30th April of that year. The valuation is required at the later of the date of purchase or 1st April 2022 followed by a further revaluation on 1st April 2027 and every 5 years thereafter. Provided that you let the property to a third party on a commercial basis, there should be no tax to pay but you still have to complete the return each year.

DISCLAIMER

The above article is provided for guidance only and may not cover your personal circumstances so you should not rely on it. It is important that you seek appropriate professional advice which takes into account your personal circumstances where you can provide the full facts of the case and all documents related to your case. Thandi Nicholls Ltd t/a uklandlordtax.co.uk cannot be held responsible for the consequences of any action or the consequences of deciding not to act.